Early retirement 101: the 85 / 90 factor – can you retire before reaching it?

(Reading time: 3:30)

Your 85 or 90 factor is like a financial security beacon, shining brightly in the retirement distance.

The closer you get to your qualifying factor, the brighter that beacon (and bigger your pension) is going to be. However, many members are deciding to retire before reaching their 85 (OTPP) or 90 (OMERS) factor. And they are doing so without realizing the kind of financial impact that decision is going to have.

But is retiring a few years shy of that magic number really going to make that much of a difference in your pension income?

Well, that fully depends on a few details beyond your 85 / 90 factor.

Educators Certified Financial Planner Lisa Raponi helps put this into perspective.

“One of the biggest financial stresses in planning for retirement is the drop in income from salary to pension, regardless if you reach your 85 or 90 factor,” explains Lisa. “That stress increases exponentially when you add in an early retirement penalty. That’s why future OTPP and OMERS recipients have to look beyond their factor in order to determine whether or not they can live off the reduced income.”

To paint a picture of the income drop Lisa is referring to, use the following calculation to estimate the amount of pension you might expect to receive in retirement:

OTPP = 2% x credited years of service x best 5-year average salary

OMERs = 2% x credited years of service x highest paid 60 consecutive months

Using the OTPP calculation as an example, let’s say you’re an education member that earned an average of $75,000 in your best five working years and maxed out your 85 factor at age 56, after 29 years of service.

2% x 29 years x $75,000 = an annual (unreduced) pension income of $43,500*

That’s a difference of $31,500 between your working years and retirement.

Now, what would your reduced pension look like if you retired before reaching your 85/90 factor?

Well that depends on your age, or how far away you are from reaching your qualifying factor. Because one of those variables will determine the extent of the penalties your pension would be hit with (for retiring early).

Those penalties are calculated as follows:

| OTPP: |

– 2.5% per each point you’re away from reaching your 85 factor; or – 5% per year you’re away from age 65 (whichever is less). |

| OMERS: |

– 5% per each point prior to the 90 factor; or – 5% per each year prior to age 65 or 30 years of service (whichever is less). |

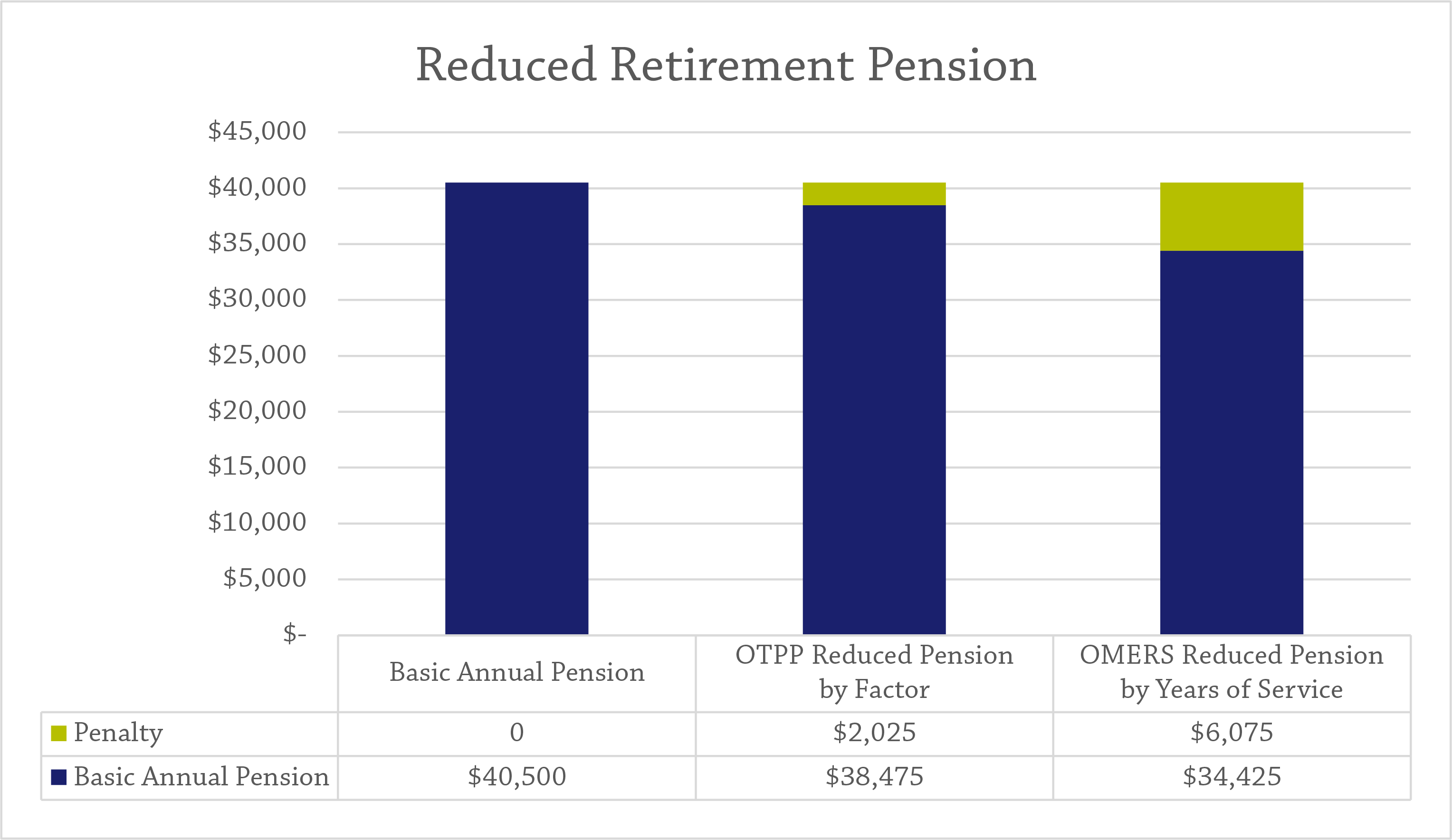

Continuing from the example above, here is the reduced retirement pension and penalty you’d be looking at if you retired two years early, based on the following assumptions:

- You’re retiring at 56 years of age

- You have 27 years of credited service

- You earned an average of $75,000 (in your 5 best years/highest paid 60 consecutive months)

In the case of OTPP, your pension is reduced by 5% (2.5% x 2) since you are two points shy of your 85 factor. For OMERS recipients, your pension is reduced by 15% (5% x 3) since you are three years away from reaching 30 years of service.

The above graph is purely for illustrative purposes. To determine the penalty you’d be looking at for your early retirement scenario, be sure to connect with an Educators financial specialist.

So, what can education members do to better financially prepare for the transition into (early) retirement?

“Well for one, don’t wait until retirement,” says Lisa. “Far too many education members hold off on making any type of plans until the day they reach their 85 or 90 factor. Trust me, you don’t want to discover that you’ll be dealing with a pension income gap at the eleventh hour. Take some time. Do a bit of research. Go into retirement with your eyes wide open and your finances in check. When in doubt, reach out to me, or any one of my colleagues here at Educators. We know your pension, both OTPP and OMERS, inside and out.”

A few more factors to consider when it comes to retiring ahead of your 85 / 90 factor:

- If you technically reach your 85 factor in the month of September of the next school year, it might make more sense to retire at the end of the current school year in June (even though it’s a few months early, it won’t make much of a difference in your pension benefits)

- If you’ve taken any approved type of unpaid leave during your education career (maternity/paternity, etc.), consider paying for your leave (I.e. buyback) before you retire, as it will increase your service credit (keep in mind this typically has to be done within 5 years of returning from a leave)

How much would a one-year leave cost you? Use OTPP’s calculator for an estimated cost (excluding interest).

Does it make sense to retire before reaching your 85 / 90 factor?

Perhaps, but let’s chat about it first. Because timing, as they say, is everything. Especially when it comes to an education member’s retirement benefits. So, before you hand in your notice, call on the financial specialists at Educators Financial Group. That way you can feel confident about making the right decision that considers both your personal and financial reasons to retire.

Book your retirement financial readiness review. And be sure to check out these topics in our Early Retirement 101 series:

*For illustrative purposes only. Login to OTPP or OMERS account for specific pension information related to your situation.